By: JD Lehman

We noted in last month’s article (link) that the bombing of Iran on February 28th began to upset the expectation that interest rates were going to come down in 2026.

April inflation readings hijacked the narrative even further as the Consumer Price Index (CPI) came in at 3.8% year over year and the Personal Consumption Expenditures Index (PCE) came in at 3.3% year over year. These readings were a 0.5% and 0.3% increase from March, respectively.

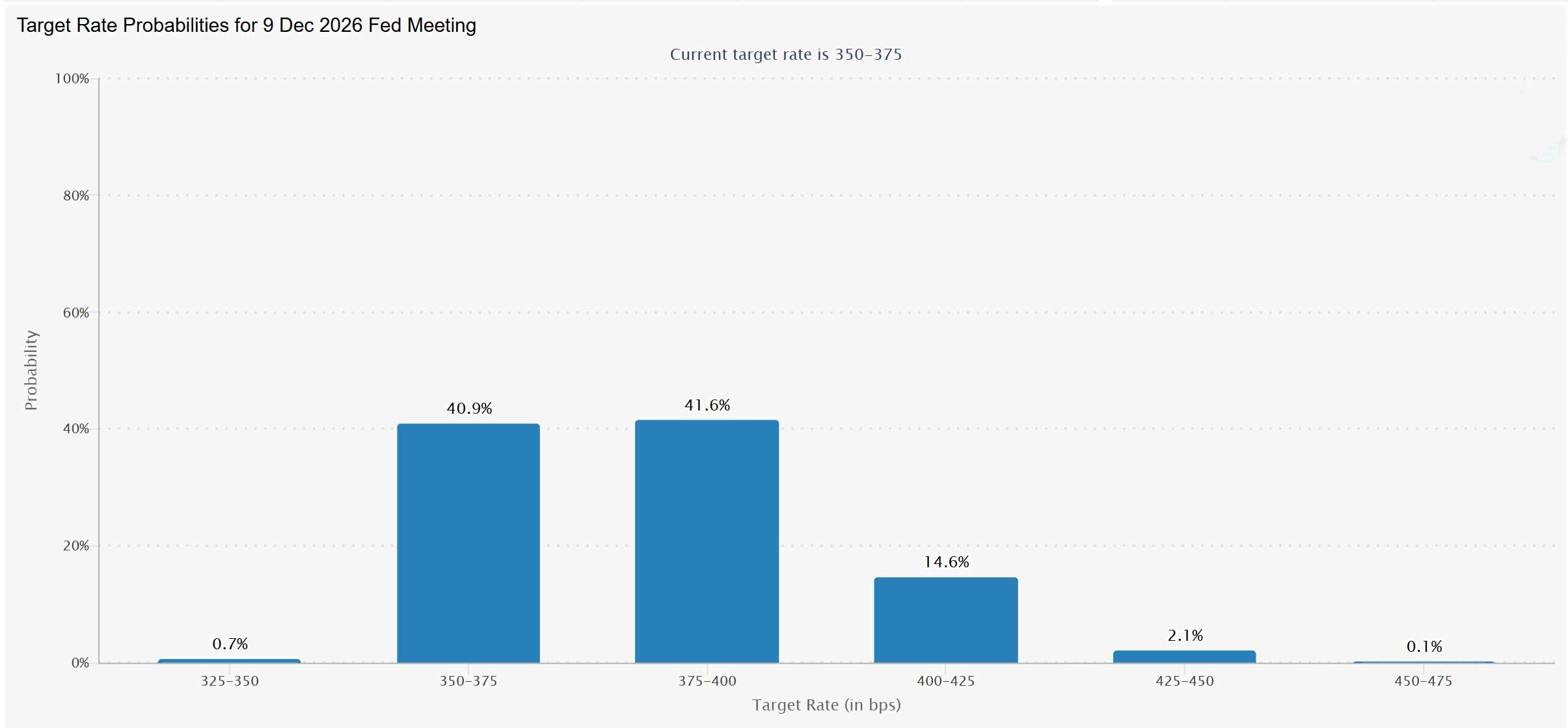

These prints threw the Treasury market into turmoil as the market hedged quickly and started to price the possibility that a rate hike could be the next move, rather than a cut. CME Fedwatch is now predicting a 40% chance that we have a rate hike by year end and almost 0% chance of a cut.

December FedWatch

– Courtesy of CME Fedwatch

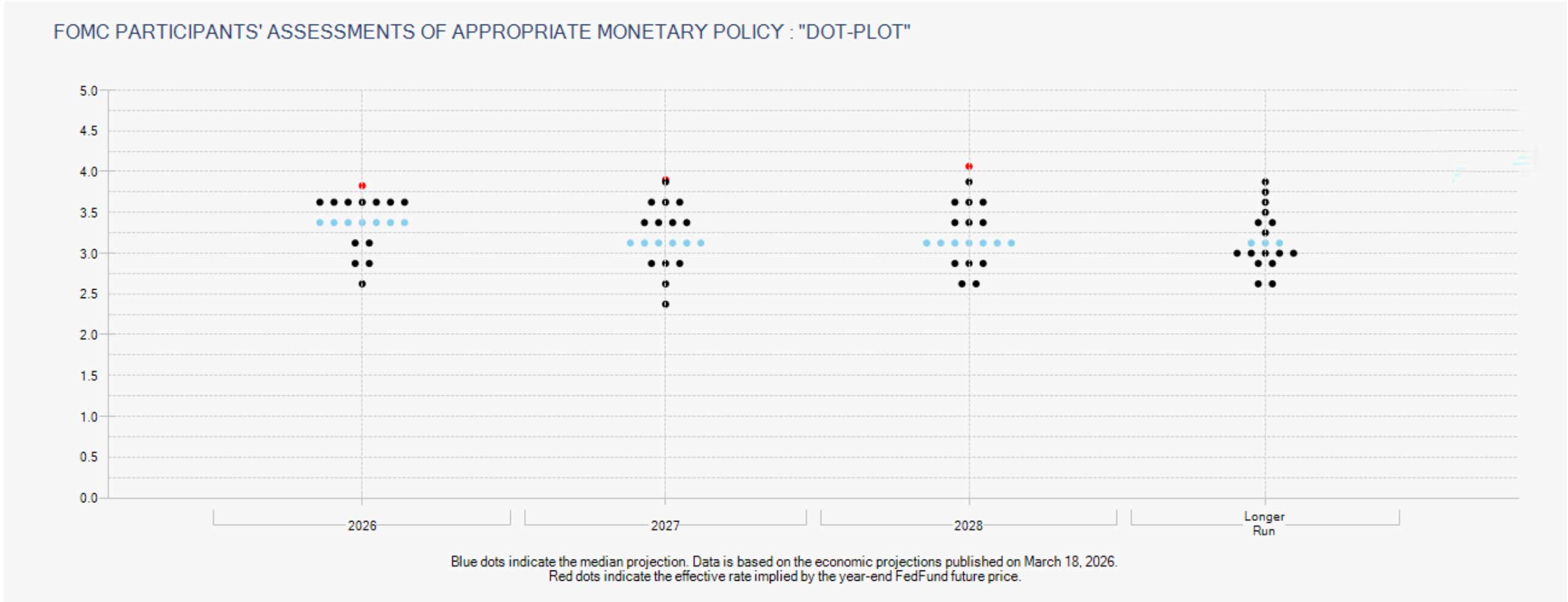

Furthermore, there is more dissent amongst the Fed Reserve as to where rates should be by year end.

Fed Dot Plot

– Courtesy of CME Fedwatch

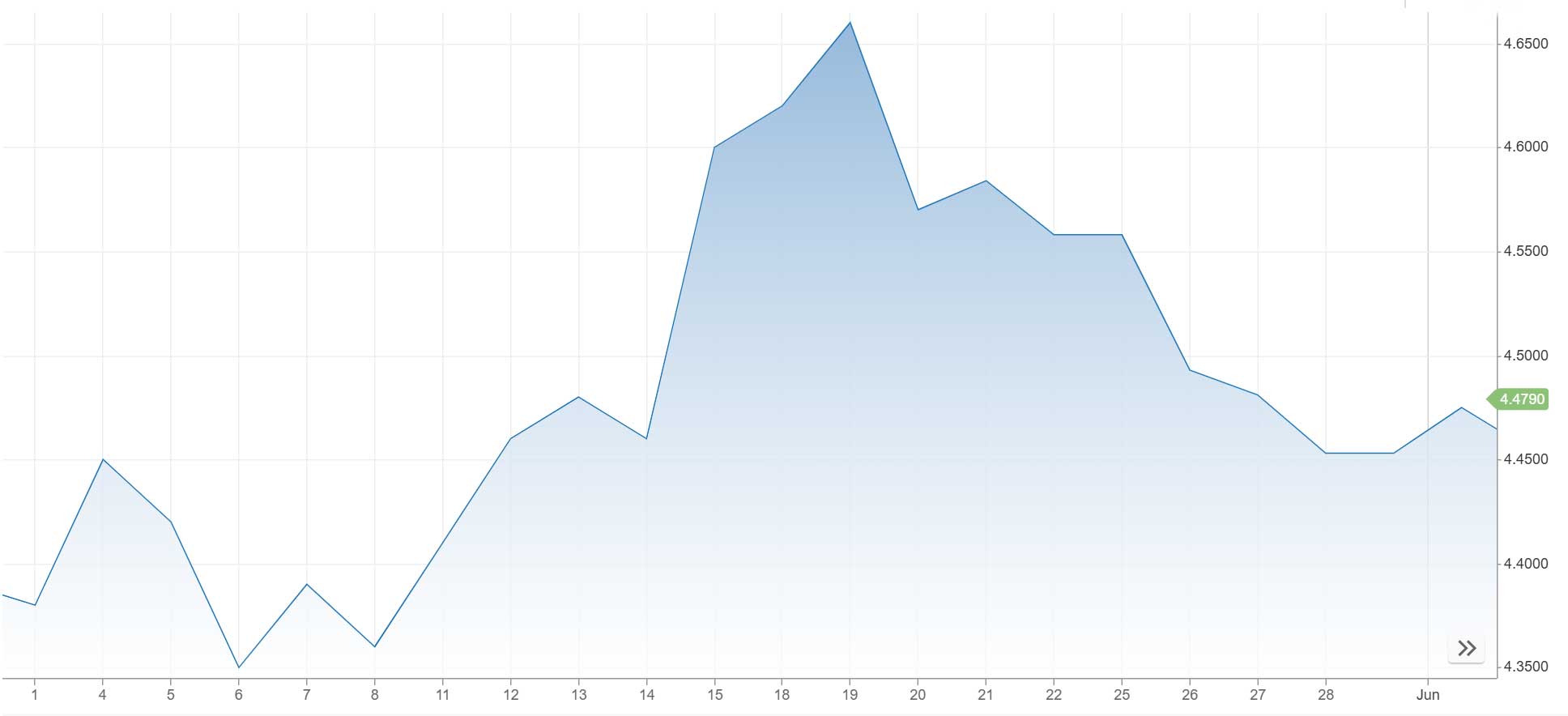

This change in narrative caused Treasury rates to skyrocket, peaking at 4.66% on May 19th, the highest reading in the last 12 months and the highest level since July 2023.

May 10-Year Treasury

– Courtesy of CNBC

As of this writing, we sit at a 4.50% 10-Year Treasury – down 16 basis points from the high noted above, but up 12 basis points from where we started the month.

Frankly, this was and is unwelcome for most of us as many were under the impression that rates were coming down in 2026 and owners could refinance or sell an asset into a more accretive interest rate environment, boosting proceeds and/or price.

What a time to be alive…

The Man of the Hour – Kevin Warsh

With all of that going on, we now have a new Chair of the Federal Reserve. Kevin Warsh was sworn in as Chairman on May 22nd. He inherits a board that is incredibly varied in their views on rates and not optimistic on a cut. He also inherits the hopes of many, including President Trump, that rates come down. Given these inflation readings, Mr. Warsh has his work cut out for him as a rate cut is not what the market expects or what the Board thinks should happen, at least while this war is ongoing.

What does this mean for CRE investors?

As we began 2026 with the expectation rates would come in, it’s hard to predict where the market is going to be by year end. The hope is this war ends and inflation comes down, but over the near term, that seems less and less likely as negotiations seem endless and oil prices remain elevated. It certainly doesn’t seem like current inflation is going to be “transitory”, meaning rates are likely higher than where we would like them to be.

Because of that, we continue to message the fact that your deal needs to work in today’s environment. Hoping for a lower rate tomorrow is not a strategy and can be incredibly fickle, but buying at a good basis in a growing market for the long term is a strategy that remains largely undefeated. And, for those with capital ready to deploy, the opportunity to buy is now as volatility limits competition. In that regard, it’s open season.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.