We’ve written about it at nauseam. We are a little tired of writing about it and imagine that you are a little tired of reading about it. That said, we would be remiss if we did not address the fact that the first rate cut is expected in… 14 days.

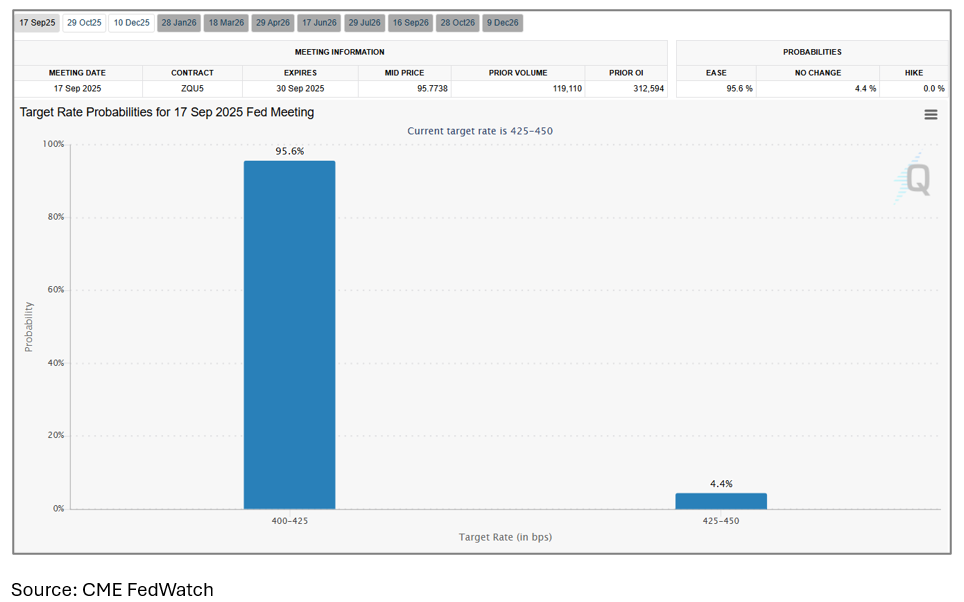

As of right now, the market has a 95.6% bet for a cut.

As you may recall from our article last month, the bond market has mostly experienced the impact of the cut already. (Link). Given this, the actual impact of the cut itself is expected to be relatively muted. What would have a bigger impact than the cut would be any hints or messaging by Fed Chair Powell as to the outlook for cuts and policy throughout the rest of 2025. That said, expectations are low for Chair Powell to give much indication as he has been rather steely in his remarks in the past, always careful not to give the market much to work with.

While we don’t expect the September cut to have much of a mathematical impact on deals, we do think that the psychological impact on the market and investors will be much greater. Knowing that we are finally going to experience some of the long-awaited easing is likely to be a welcome relief to the market, which may increase transaction activity despite not having much of an impact on the numbers.

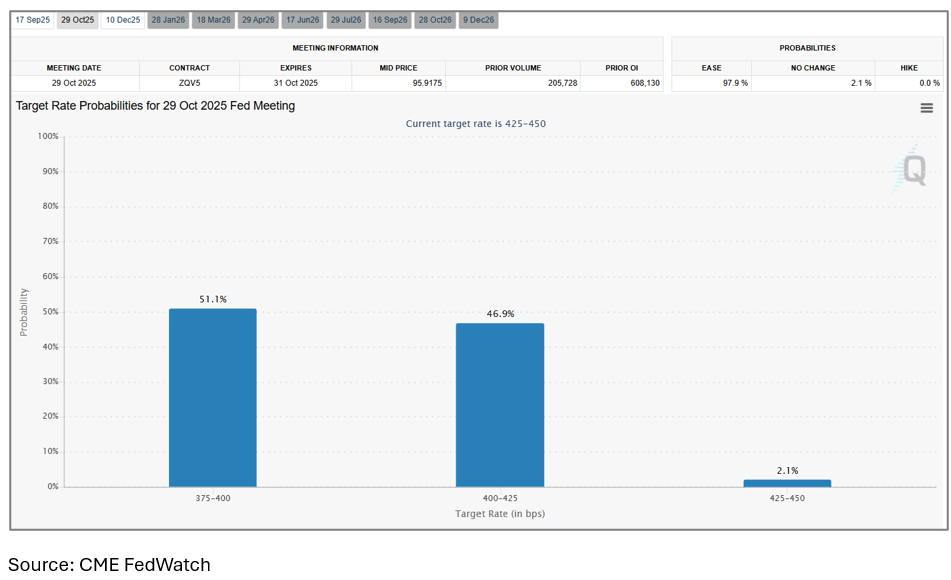

While plenty of economic data will come out after the September meeting that will have potential to move the market, investors won’t have to wait long for the next major event as the Fed’s following meeting will be six weeks after the September meeting, occurring on October 28th – 29th. In addition to potential policy changes and additional rate cuts, the Fed will release their updated dot plot at the October meeting, which will further signal to the market the Fed’s expectation of where rates will be over the longer 12-month outlook. As of today, the market has close bets on whether there will be a second cut in October (51.1%) or if the Fed will hold steady after one cut (46.9%), with the remaining 2.1% chance of bets that the Fed will not cut in September or October.

One other X-factor at play is the expectation that President Trump will announce his choice to replace Jerome Powell as Fed Chair. While Chair Powell’s term is not up until next May, there is a chance that the new Chair-Elect will have a shadow affect on the market, and that the market will start to move based on the hawkishness or (more likely) dovishness of the candidate’s expected stance.

Between tariffs, revised survey responses, Fed firings, and lawsuits embroiled in almost all of these matters, it has been really difficult to know what to expect. That said, we ae bullish on the first rate cut of the year happening in September. Beyond that, our hope (and anticipation) is that data continues to come in that would support at least one more cut in 2025, and that the market aligns with the expected policy of the new Fed Chair-Elect, in which case we think would provide a very favorable environment for transactions. Beyond the actual mathematical impact to deals, knowing that we are headed into a prolonged cycle of easing will provide the tailwind that the market really needs.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.