Last week, the Federal Open Market Committee (FOMC) cut the federal funds rate by 25 basis points, bringing the target range down to 3.75%–4.00%. The move was widely anticipated, but bond yields edged higher across the Treasury curve after the announcement as markets adjusted expectations for additional cuts in December and January.

During his press conference, FOMC Chair Jerome Powell emphasized that “a December cut is not a foregone conclusion.” He noted that committee members engaged in a spirited debate over future policy—particularly regarding a potential December cut—given the mixed economic signals of slightly higher-than-expected inflation and uncertainty in the labor market. Adding to the challenge, the ongoing government shutdown has delayed the release of key economic data the Fed typically relies on to guide decisions.

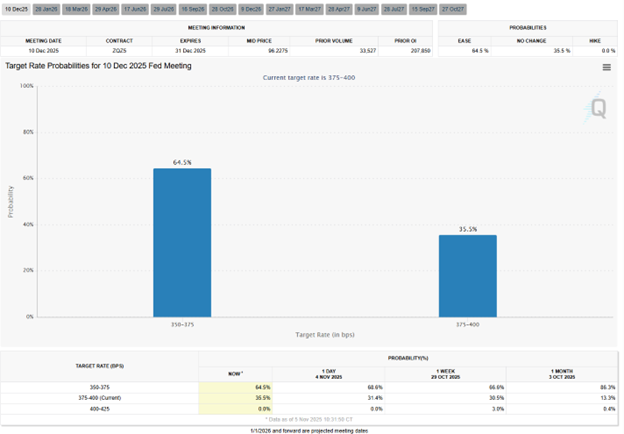

Prior to Powell’s remarks, the 10-year Treasury yield hovered around 4.00%, with markets pricing in roughly a 96% probability of a December rate cut. After his comments tempered those expectations, yields rose modestly, and the 10-year settled near 4.10%. Market-implied odds of a December cut have since fallen to about 64.5%, and the 10-year appears to have stabilized around that level.

One encouraging takeaway for investors came from Powell’s comments on the Fed’s balance sheet strategy. The Fed announced it will stop purchasing mortgage-backed securities (MBS) and instead replace maturing MBS holdings with Treasuries. Since June 2022, the Fed has been operating under a quantitative tightening (QT) program, reducing its balance sheet, which it now plans to conclude by December 1, 2025.

This shift is broadly positive for rate-sensitive investors. As the Fed transitions to becoming a significant net buyer of Treasuries, demand for government bonds should increase, helping to suppress yields and ultimately lower borrowing costs. While the Fed’s prior MBS purchases supported mortgage and lending spreads, the new focus on Treasuries may produce an even more favorable overall effect on interest rates.

Historically, government shutdowns have had minimal lasting effects on interest rates. However, the current shutdown—now entering its 36th day—is on track to become the longest in U.S. history, and its prolonged nature raises the potential for meaningful market impact.

If the Fed concludes that the lack of economic data limits its ability to make informed policy decisions, it could decide to pause rate changes, introducing further uncertainty and upward pressure on yields. Conversely, if the shutdown materially weakens economic activity, investors would likely seek safety in Treasuries, driving rates lower.

That said, neither outcome is desirable. Prolonged uncertainty and volatility benefit few market participants. The old adage still applies:

“You can make money on the way up, and you can make money on the way down—but it’s hard to make money when you don’t know where you’re going.”

For commercial real estate participants, the current environment underscores the importance of timing and flexibility. Borrowers may see opportunities to lock in more favorable rates in the near term if yields hold steady or decline, while investors should continue to monitor Treasury movements closely as a signal of market sentiment and potential cap rate adjustments.

While uncertainty remains, the Fed’s evolving stance toward balance sheet normalization and Treasury purchases suggests a gradually improving rate environment over the coming quarters. Staying disciplined—evaluating deals based on fundamentals rather than short-term volatility—will remain key to navigating this period successfully.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.