November 6, 2024 – On the same morning that the 2024 Presidential election was called for Donald Trump, Treasury Rates across the yield curve moved materially higher. Intra day as of 8:30am, the 5-Year Treasury Yield rose by 10 bps to 4.27% and the 10-Year Treasury Yield moved 15 bps higher to 4.44%. This move comes not only after the presidential election was called for the republican candidate, but in what appeared to be a toss-up election where republicans have now gained control of the Senate and maintained control of the House of Representatives.

Pundits will speculate, but it seems difficult to determine in the near-term if the election has any material impact on this move, or if this move was already in motion prior to the election announcement. Another major event this week that also impacts bond rates is the Federal Reserve Open Market Committee (“FOMC”) meeting, which will be held today and tomorrow, with policy announcements made on November 7th at 2pm. It is not abnormal for material moves to start to occur in the days leading up to a FOMC meeting as market hedges are placed by those trying to determine what the FOMC conclusions will be.

Some feel as though the market has been playing a game of chicken with the Federal Reserve. Treasury Yields moved materially higher after the FOMC’s September meeting where they cut rates for the first time since they started their raising cycle in April of 2022 and laid out a path of future cuts through 2027. That said, other experts have stated that the upward movement in Treasuries is simply a function of the normalizing and steepening yield curve as well as normalizing market conditions. The expectation by markets has been that Treasury Rates will continue to move higher in the face of Fed Funds Rate cuts.

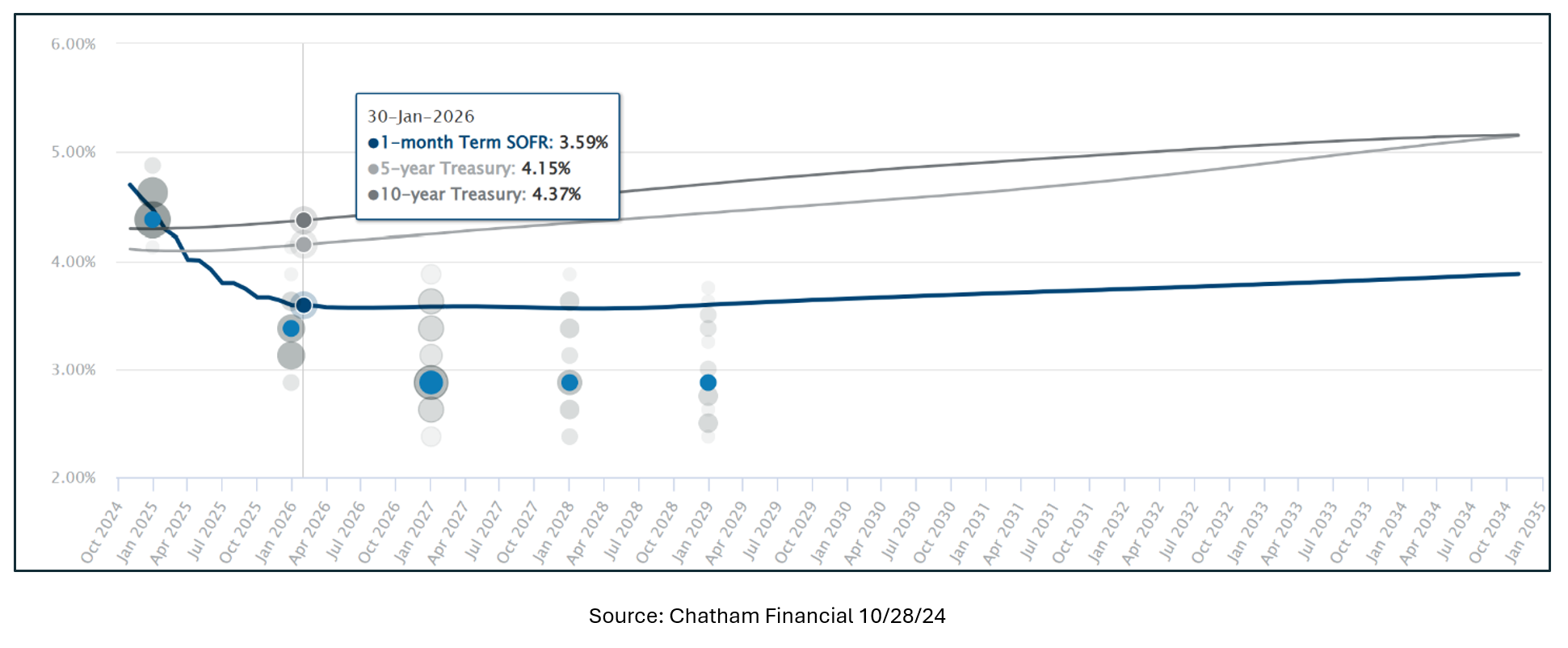

Of note, prior to the election results and as of October 28, 2024, the forward curve for the 5- and 10-Year Treasury for January 2025 were 4.09% and 4.29% respectively. This is with the expectation of an additional 50 bps of cuts by the FOMC to the Fed Funds Rate by that same time.

Looking further out to January 2026, the forward-curve of the 5- and 10-Year Treasury are 4.15% and 4.37%, respectively. These projections are expected at a time with an effective Fed Funds Rate of 3.25% – 3.5%, which is 75 – 100 bps below the January 2025 projection.

Leading up to the election many argued that economic policies of both presidential candidates were inflationary and would put upwards pressure on rates. With a Republican Sweep in the election, it certainly appears that the agenda has the ability to be put in place unabated by an otherwise split congress. Other experts and media personalities have stated that the projection of the deficit and current and forecast debt to GDP ratio is ultimately putting upward pressure on rates and is expected to create a lack of demand for US Treasuries.

Whether or not the election had a material impact on the move in rates, or if this movement is within the range of normal short-term volatility in what is otherwise an expected steady increase in rates, we may not be able to determine. What is absolutely true, is that that whatever administration was elected to office was going to have to face some hard challenges ahead balancing both monetary and fiscal policy in the face of the national deficit and forecasted debt to GDP. As it relates to commercial real estate, investors should heed the forward curve and understand that for the time being, all expectations are continued increases in long-term interest rates.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.