By: Scott Williams

The recent and ongoing conflict in Iran has certainly added a new layer of uncertainty to financial markets. Historically, geopolitical events in energy-producing regions have had the potential to influence inflation expectations and bond markets through their impact on oil supply and pricing. Beyond the humanitarian concerns and the general destabilizing effect of a conflict of this nature, the primary concern for investors is that a sustained increase in the price of oil could make the already persistent inflation problem even tougher.

In the early days following the escalation, markets did experience the type of volatility often associated with geopolitical shocks. Oil prices moved higher, and Treasury markets saw short-term swings as investors evaluated the potential impact on energy supply and inflation.

Notably, however, the 10-year Treasury had already been trending lower in the days leading up to the conflict, briefly falling below 4% and reaching 3.97% on February 27 before the first strikes began, matching the 52-week low. Since then, yields have largely returned to similar levels, suggesting that while geopolitical risk introduced volatility, it has not materially altered the broader trajectory for long-term interest rates.

Because energy prices feed directly into inflation expectations, geopolitical conflicts involving major oil-producing regions can influence how markets think about the Federal Reserve’s next move. If oil prices were to rise meaningfully and remain elevated, the Fed could face a more complicated policy environment, particularly if inflation shows signs of stabilizing above the central bank’s target.

For now, however, markets appear to be treating the conflict as a conditional risk scenario rather than a base-case economic shift. Rate futures continue to imply the possibility of easing later in the year, though the timing and magnitude of those cuts remain subject to incoming inflation and economic data.

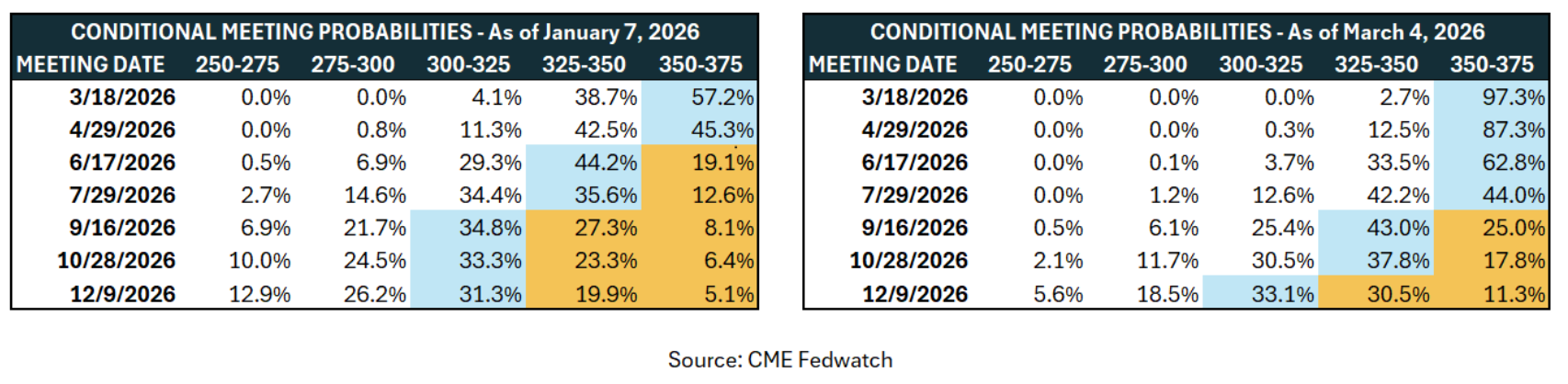

Market projections for rate cuts in 2026 have shifted since January. The primary change has been pushing the expected timing of the first cut from June to September 2026, while the probability of two cuts instead of one has narrowed.

While the geopolitical backdrop has added uncertainty, it has not yet significantly changed the market’s expectations for the overall rate cycle.

For commercial real estate investors, the key takeaway is that rate stability has persisted despite the geopolitical headlines. Over the past several years, transaction activity has often been influenced less by the absolute level of interest rates and more by the volatility surrounding their direction. The relative lack of volatility given the implications of the current conflict is somewhat surprising but also reassuring.

The fact that the 10-year Treasury has largely returned to its pre-conflict levels suggests that capital markets continue to view the underlying macro environment as broadly stable, at least for the time being. If that stability persists, it may provide a more constructive backdrop for underwriting and transaction activity as investors gain greater confidence in rate expectations.

While geopolitical developments can create short-term disruptions in financial markets, their longer-term impact often depends on whether they translate into sustained changes in inflation, energy supply, or economic growth.

At this stage, the bond market appears to be signaling that the conflict has introduced uncertainty, but not yet a structural shift in the rate outlook. For investors closely watching the trajectory of interest rates, the key variables remain largely unchanged: inflation trends, economic data, and the Federal Reserve’s evolving policy path.

In the meantime, the resilience of the 10-year Treasury following the initial volatility may be one of the clearest signals that markets still expect the broader rate environment to remain relatively stable as the year unfolds.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.