By: JD Lehman

Though Greenville and the Southeast (and most of the Eastern US) got hit with very cold temperatures throughout January, the year started off hot from an economic news standpoint. Stock market growth and volatility, a Fed press conference, Davos, tariffs, Greenland, and Chair Powell’s replacement was named. Can AI even keep pace?

Though the Fed stopped lowering rates and kept the Fed Funds rate between 3.50% – 3.75%, the 10-year Treasury rate increased by about 8 bps throughout the month, closing the month at 4.24%. It still proves to be the case that “Good news is bad and bad news is good” from an interest rate standpoint. In Powell’s press conference, he mentioned that the “outlook for economic activity has improved, clearly improved since the last meeting, and that should matter for labor demand and for employment over time”. Powell is noting that unemployment is hovering around 4.5% and annual inflation is in the 2.7% – 2.8% range.

Chair Powell further noted “And, again, we think our policy is in a good place … I just would say that I’m not making a judgment about how one of them [inflation and unemployment] is more at risk than the other, just that the risks to both of them have diminished.” Based on the recent data, it would appear he is correct.

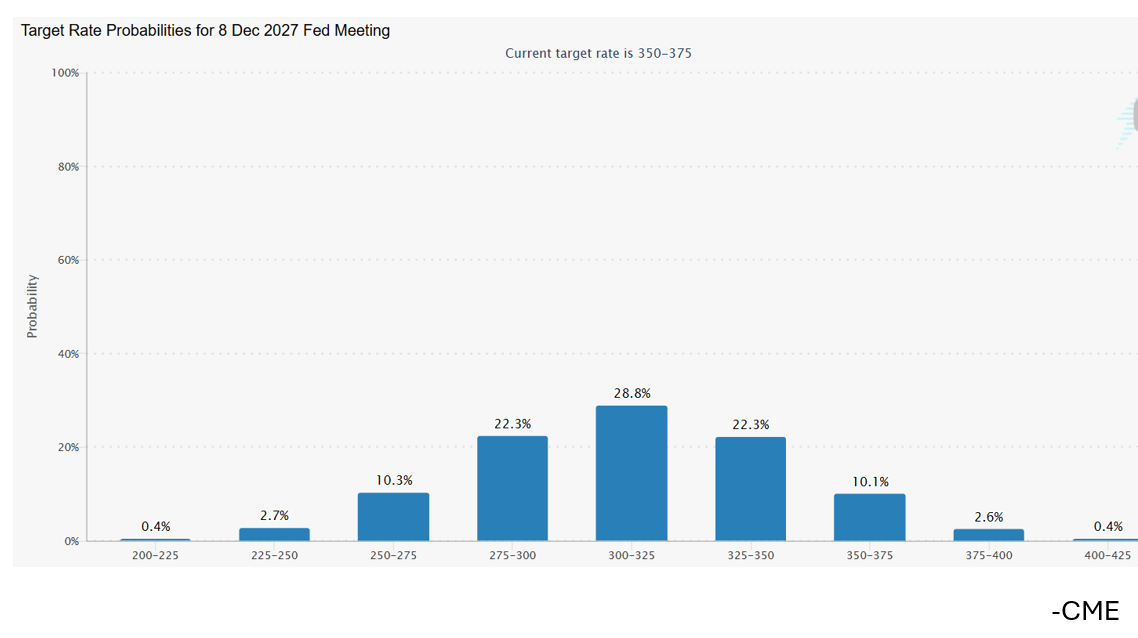

The Fed Funds Rate is in a neutral range now, and it appears that will be the case throughout ‘26. Currently, the market is banking on one to three 0.25% cuts this year, as evidenced by the below chart:

We see the Treasury market already pricing in these moves so there likely won’t be much of an effect on Treasury rates.

President Trump announced on Friday, 1/30, that Kevin Warsh would be replacing Jerome Powell as head of the Federal Reserve. Though the Senate will need to confirm this appointment, Mr. Warsh’s tenure will likely begin in May. A noted inflation hawk, Mr. Warsh also believes in substantially shrinking the Fed’s balance sheet, as it currently owns a substantial amount of U.S. Treasury bonds. While President Trump has been shouting for interest rates to be lowered, shrinking the Fed’s balance sheet will likely counteract any effect of future rate cuts. Thinking of supply and demand, if the Fed sells these bonds, supply increases and demand drops, meaning the price of the bond will drop and the corresponding yield / rate will rise. Bond yields move opposite of pricing.

As stated earlier, we believe we are where we are from a rate standpoint and that current rates are at a point that allows Borrowers to obtain credit at a cost that is accretive to their bottom line. We try not to message a dream that we doubt will occur but want to think critically about the environment we’re in and the data we’re seeing. The current landscape doesn’t seem to necessitate much movement from where we are as the US economy is in good shape. Thus, I think we’ll continue to see Treasury rates around 4%. The opportunity then is to capitalize on the trillions in debt that will mature throughout 2026. This will create opportunities for buyers as these maturities will force a decision to sell and in some instances, realize a loss for both a seller and/or a lender. It’s a great opportunity for a basis to get reset and set up potential for appreciation.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.