Markets have spent much of 2025 anticipating some degree of monetary policy relief. With inflation showing signs of resilience and global uncertainty rising—driven in part by escalating tariffs, the Federal Reserve has remained cautious. However, the labor market appeared too strong to justify rate cuts, at least on the surface. That narrative began to unravel last week.

The July employment report from the Bureau of Labor Statistics (BLS) fell notably short of expectations, with only 73,000 jobs added, compared to projections north of 100,000. That said, it was not the headline number that captured market attention—it was the substantial downward revisions to prior months. May and June employment figures were revised down by a combined 258,000 jobs, effectively signaling that labor market strength had been materially overstated.

Up until this report, the Fed had limited justification for rate cuts. While core inflation was cooling modestly, wage growth and jobs data suggested a still-resilient economy. In this environment, policy easing risked stoking inflationary pressures. However, the new labor market data changes that calculus.

Critically, this is not just about a single weak report—it’s about the reliability of the data that policymakers and markets have been relying on for months. The revelation that employment growth has been consistently overestimated undermines the Fed’s assumption that the labor market remains “too strong” to warrant rate cuts.

We frequently hear from real estate investors that they are waiting for a rate cut and we are constantly reminding them that while rate cuts matter, what really matters for CRE investing is the 5- and 10-year treasury rates. Following the BLS report, yields across the curve fell sharply- approximately 20 basis points on both the 5- and 10-year treasury.

This swift repricing reflects a core truth about fixed income markets: the news is the move. In other words, it is not only policy that drives bond yields, but the shift in expectations around policy. For all of those investors waiting around for the Fed’s 25 basis rate cut, we all but got it last week.

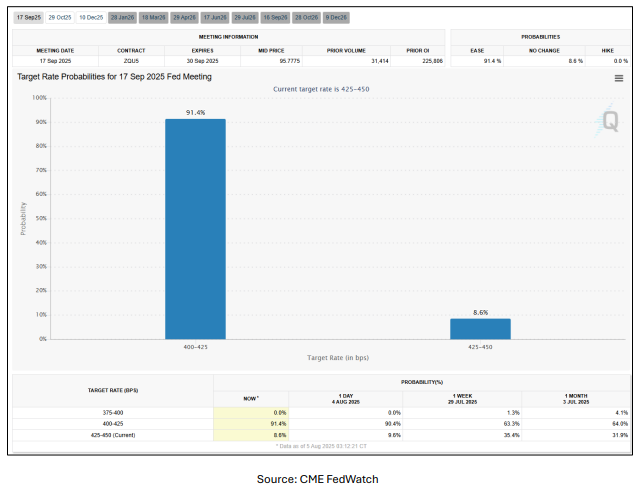

The move in yields was reinforced by a surge in market-implied rate cut probabilities. According to the CME FedWatch Tool, the likelihood of a September rate cut rose from approximately 65% prior to the report to over 90% in the immediate aftermath.

This repricing reflects the market’s belief that the Fed now has sufficient cover to begin easing—something investors have been signaling a desire for over the past several months.

If this past week revealed anything, it’s that revisions matter, and sometimes more than the initial print. Whether the Fed chooses to act in September will depend on forthcoming inflation and employment data, but as far as the market is concerned, the pivot has already begun.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.