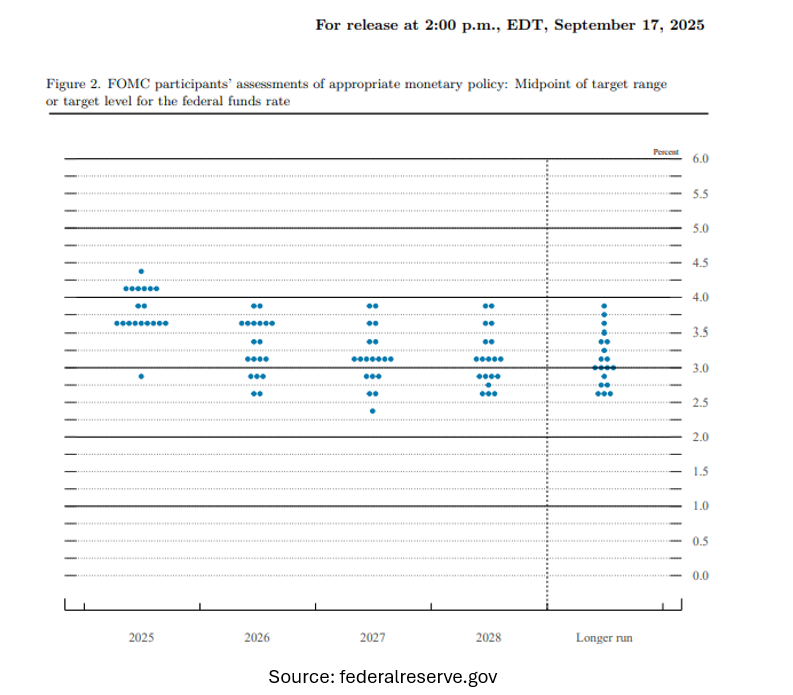

On September 17th the Fed delivered the first rate cut of 2025. In addition to the cut the Fed released an updated dot plot where 9 of the 19 voting members projected two additional cuts for the year, making that the mean projection and most likely scenario.

Two additional cuts have become the base expectation for the market, evidenced by a 99.0% chance of a cut in October and an 86.9% chance of a cut in December, according to CME FedWatch data.

The bond markets reacted favorably to the cut, with the 10-year Treasury briefly dipping below 4.0% to 3.99%, before returning to 4.11% the following day. While the 10-year has settled in between 4.10% and 4.18% in the weeks following the cut, dipping below 4.0% is significant as that is the first time we have seen rates below 4.0%. since October of last year.

Data has been finicky since the cut, with inflation data in the past two weeks coming in mostly higher than expected, and jobs reports being unclear, with the latest revision in the ADP jobs reports being revised below expectations and showing the largest decline in payrolls in over two years (Link). The Government also shut down effective today. Historically, shutdowns have had a limited or short-lasting impact on Treasury rates, but the impact that they do have is generally to trend rates downward given the softness and uncertainty that the shutdown creates. If there was any question as to whether the sticky inflation data was enough to overcome the weak labor market data, perhaps the Government shutdown will just add enough to clear the way for the Fed to continue to make their two additional cuts this year as expected.

We do not want to understate the impact (help) these cuts will have on the lending market, as the lowering of short-term rates will help spur activity, but as we say time and time again, the 10-year treasury has the largest impact on CRE values and permanent lending rates, and the long-end of the curve is being stubborn in the face of the cuts. It is becoming more clear that the market appears more concerned with other issues like deficit spending, the national debt, and geopolitical conflict, than it is with short-term policy and outlook. It will be very interesting to see if there is any data or moves the Fed can make to further make an impact on the benchmark bond rates, or what it will ultimately take to ease the long end of the curve.

While additional relief for CRE investors may be uncertain, we have had substantial relief in the 10-year throughout the year, falling from as high as 4.78% in January to 3.99% and settling in the 4.10% – 4.18% range. This is substantial relief and is enough to help some investors bridge the gap they’ve been needing for some time. Additionally, floating rates will continue to come down, which will help transitional and bridge plays as well as development.

So, while the Fed’s rate cuts and the subsequent market reactions provide some relief, particularly for CRE investors and those relying on floating rates, the broader impact remains uncertain. Persistent concerns over long-term issues like deficit spending, national debt, and geopolitical tensions continue to overshadow short-term monetary policy. As the year progresses, it will be critical to monitor whether the Fed’s actions can meaningfully influence the stubborn long end of the curve or if external factors will dictate the path forward for the lending and investment landscape.

Partner with us to navigate the complexities of commercial real estate. Get in touch today to explore how our expertise can unlock the full potential of your real estate investments.